Cobalt’s Recovery: Strong Demand, Constrained Supply

A Market Transformed

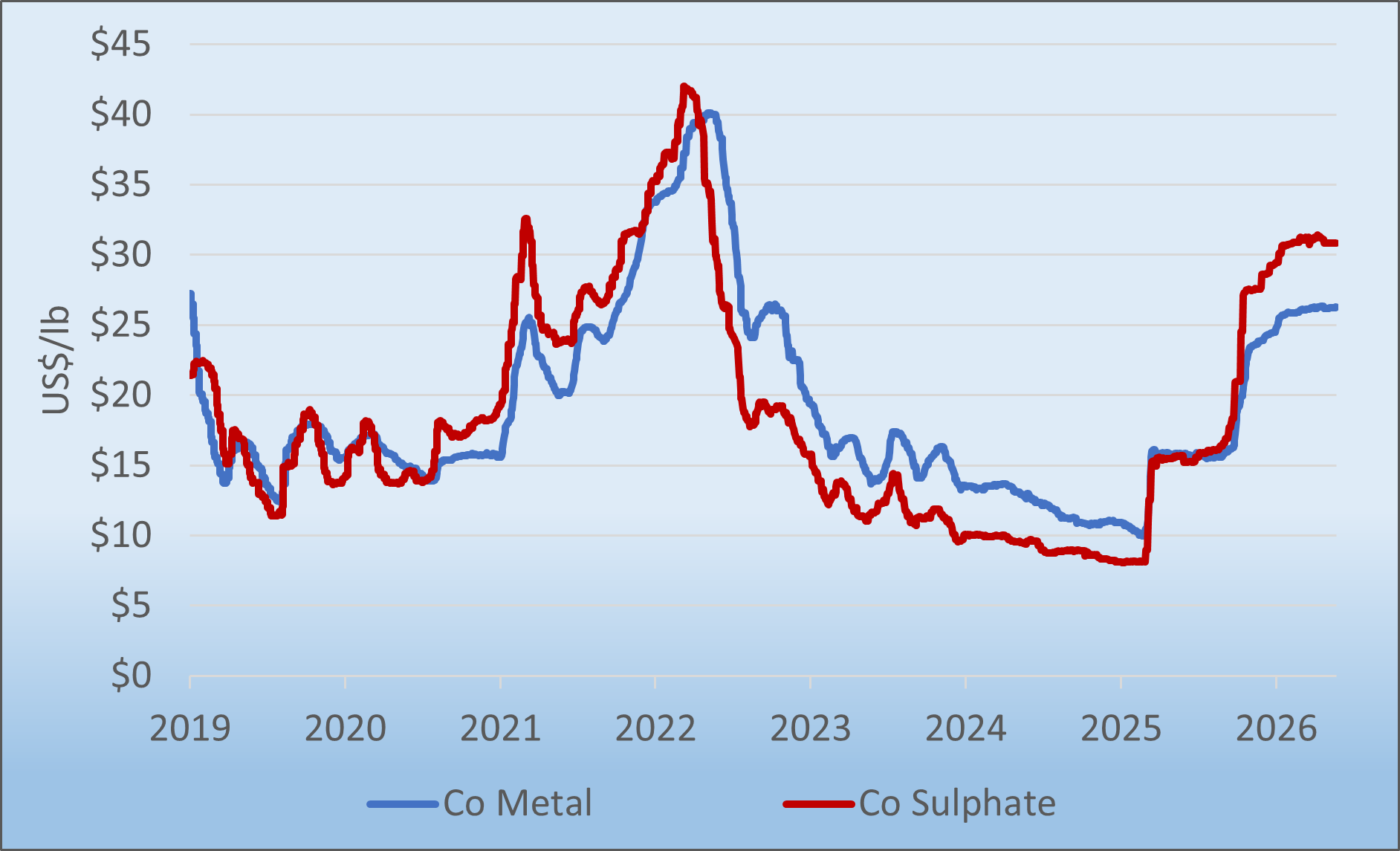

The cobalt market has undergone a remarkable reversal. After hitting multi-year lows in 2024, cobalt metal prices have staged a sustained recovery. The metal has averaged US$26/lb year-to-date in 2026, more than double the 2024 average. Meanwhile, cobalt sulphate is currently trading around US$31/lb on a Co-equivalent basis, reflecting firm downstream demand for battery-grade material.

The recovery reflects a confluence of structural forces: the DRC government's moves to manage supply, a surge in EV adoption, and intensifying geopolitical pressure on critical mineral supply chains.

Source: Fastmarkets, Cobalt Blue Holdings

EVs Accelerate — and Cobalt Comes With Them

EV sales are running at a record pace, up 6% year-on-year at around 1.6 million units per month. The catalyst is as much geopolitical as technological: US strikes on Iran in February triggered a renewed oil price shock, and history shows that every major oil shock dating back to the 1970s has driven fundamental shifts in how automakers operate. The current disruption looks set to follow the same pattern.

The EV surge has injected momentum across battery materials markets. Lithium has recovered from cyclical lows on the back of booming battery demand, including grid-scale storage driven by AI data centre growth, and cobalt is now following suit.

Battery chemistry remains an important nuance. LFP batteries — cheaper and cobalt-free — have over the past four years captured the dominant Chinese EV market and now account for the majority of stationary storage globally. NMC remains the chemistry of choice for premium, long-range vehicles, supporting ranges of 600–1,000km versus LFP's typical 400–500km. The divide is clear: LFP for volume and durability; NMC for performance.

A further dimension favours NMC specifically in Europe. EU battery regulation mandates that from set thresholds, rising progressively over time, a defined proportion of key materials in new batteries must come from recycled sources. NMC chemistry, with its cobalt, nickel and manganese content, lends itself to economically viable recycling. LFP, by contrast, is rarely recycled: iron phosphate inputs carry too little value to justify the process. As recycled content requirements tighten, LFP faces a structural compliance headwind in European markets that NMC does not.

Supply Under Pressure

The demand recovery is colliding with a fragile supply landscape.

DRC export restrictions remain a defining feature. The country produces over 70% of the world's mined cobalt, and the quota and export licensing regime introduced in 2025 continues to constrain supply. Uncertainty around allocations has kept buyers cautious and inventories tight.

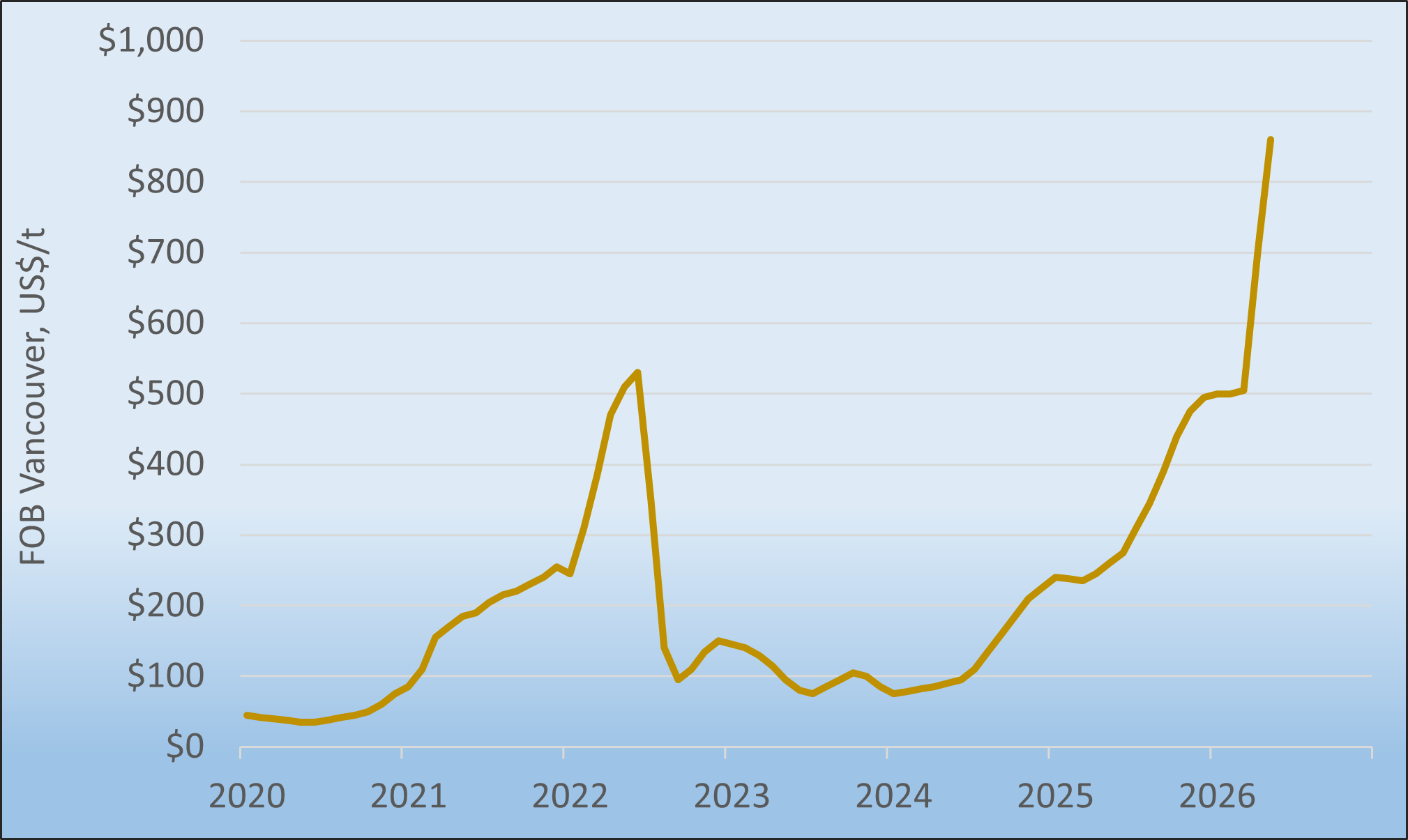

Sulphuric acid is emerging as a critical bottleneck extending well beyond cobalt. Some 80–90% of DRC cobalt production imports acid from the Middle East, a dependency shared across many mining jurisdictions. With the Strait of Hormuz under pressure following the US-Iran conflict, portions of that supply chain are at risk.

Source: CRU, Argus, Cobalt Blue Holdings

The same sulphur shortage is biting in Indonesia, where HPAL operations rely heavily on imported sulphur and China's sulphuric acid export ban has compounded the pressure. Zhejiang Huayou Cobalt's Huafei HPAL operation has already cut capacity by approximately 50% in response — a significant signal for both nickel and cobalt byproduct supply. Rising production costs are improving the conditions for Australian nickel-cobalt restarts.

Sherritt International's Cuba exit adds a further supply dimension. Sherritt suspended all Cuban joint venture operations on 7 May 2026 following the Trump administration's secondary sanctions executive order, ending a 32-year presence. In 2025, Sherritt accounted for 5% of global cobalt metal production, and its Fort Saskatchewan refinery represented 19% of LME-approved Class 1 nickel briquette output. That volume will not be easily replaced.

The Supply Chain Imperative

The events of 2025 and 2026 have made one thing impossible to ignore: the battery and critical minerals supply chain cannot be built on geopolitical assumptions that no longer hold. Concentration risk in the DRC, dependence on Middle Eastern acid and elemental sulphur, and the vulnerability of Chinese-controlled processing capacity are not abstract concerns, they are live constraints affecting production today.

The build-out of Western and allied supply chains, from mine to cathode to cell, requires an integrated approach combining policy, capital, and technology, developed at scale and with urgency.

Cobalt Blue's Position

Cobalt Blue is positioned at the intersection of these forces. The first priority is the Kwinana Cobalt Refinery (KCR), Australia's first dedicated cobalt refinery. As non-Chinese gigafactories scale up NMC and NCA cell production, demand for battery-grade cobalt sulphate outside China is growing rapidly. KCR is designed to meet that demand: a versatile, multi-feedstock facility capable of producing high-purity cobalt sulphate for the battery industry and high-grade cobalt metal for advanced manufacturing and defence applications. Recent technical milestones and successful product qualification have validated the design, attracted international partner interest, and reinforced the project's development pathway. Getting KCR into production is a clear near-term priority.

The second imperative is the Broken Hill Cobalt Project (BHCP). BHCP hosts one of the largest cobalt deposits outside the DRC, geologically distinct from the sulphide and laterite deposits that dominate global supply. Critically, BHCP is free from the acid import dependency that is now constraining DRC and Indonesian producers. Bringing BHCP into production would establish a fully integrated, mine-to-refinery cobalt supply chain on Australian soil: sovereign, reliable, and aligned with the needs of Western battery manufacturers seeking alternatives to DRC-origin material.

In a market where provenance, supply security, and processing independence are no longer secondary considerations, Cobalt Blue's integrated project model is increasingly relevant.