Why the world needs cobalt now more than ever

Once overlooked by critical minerals investors, cobalt now sits at the intersection of two forces rewriting the global economy: an accelerating clean energy transition and an unprecedented supply shock from the world's dominant producer.

Cobalt is the unsung backbone of modern civilisation. It is central to the lithium-ion batteries powering electric vehicles and grid-scale energy storage, to the electronics underpinning our connected society, and increasingly to the infrastructure supporting artificial intelligence. Yet for years, cobalt was easy for investors to ignore - mined supply was in vast oversupply and prices were depressed.

That era is over. Two converging forces, a resurgence in EV demand and a dramatic shift in supply availability from the Democratic Republic of Congo, have fundamentally altered the cobalt outlook. The question is no longer whether the world needs cobalt. The question is whether the world can get enough of it.

The oil shock changes the EV calculus

Rising petrol prices have a way of concentrating minds. The recent oil shock has pushed fuel costs back to the front of consumer consciousness, prompting many to reconsider electric vehicles — not just as an environmental statement, but as a practical and economic decision. Crucially, this is a calculation being made not only for today, but for the inevitable price volatility of the future.

Car makers, having spent several years trimming EV pipeline ambitions as growth forecasts softened, are now revisiting those decisions. The timing matters: unlike even three or four years ago, consumers are now spoiled for choice in available and affordable EV models.

This sentiment shift is consequential for the cobalt market. After several years of downgraded forecasts, EV and battery market analysts are beginning to revise projections upward once more. More EVs on the road means more lithium-ion batteries. More batteries means substantially more cobalt demand.

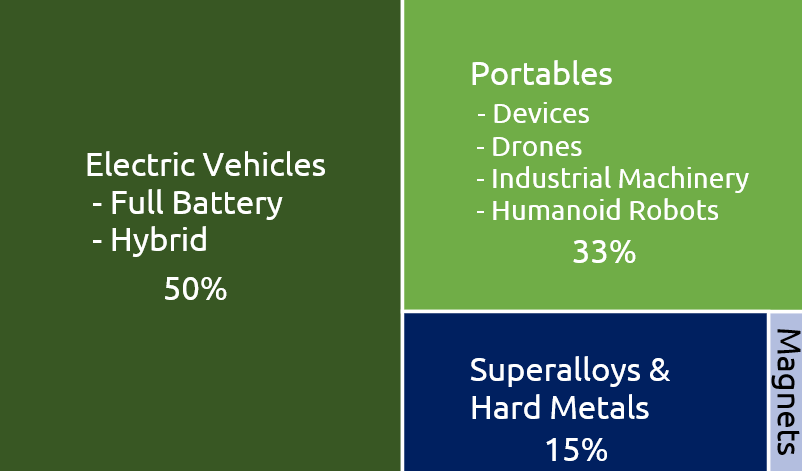

COBALT DEMAND BY END USE — SHARE OF TOTAL CONSUMPTION

Source: Benchmark Minerals, Cobalt Blue Holdings

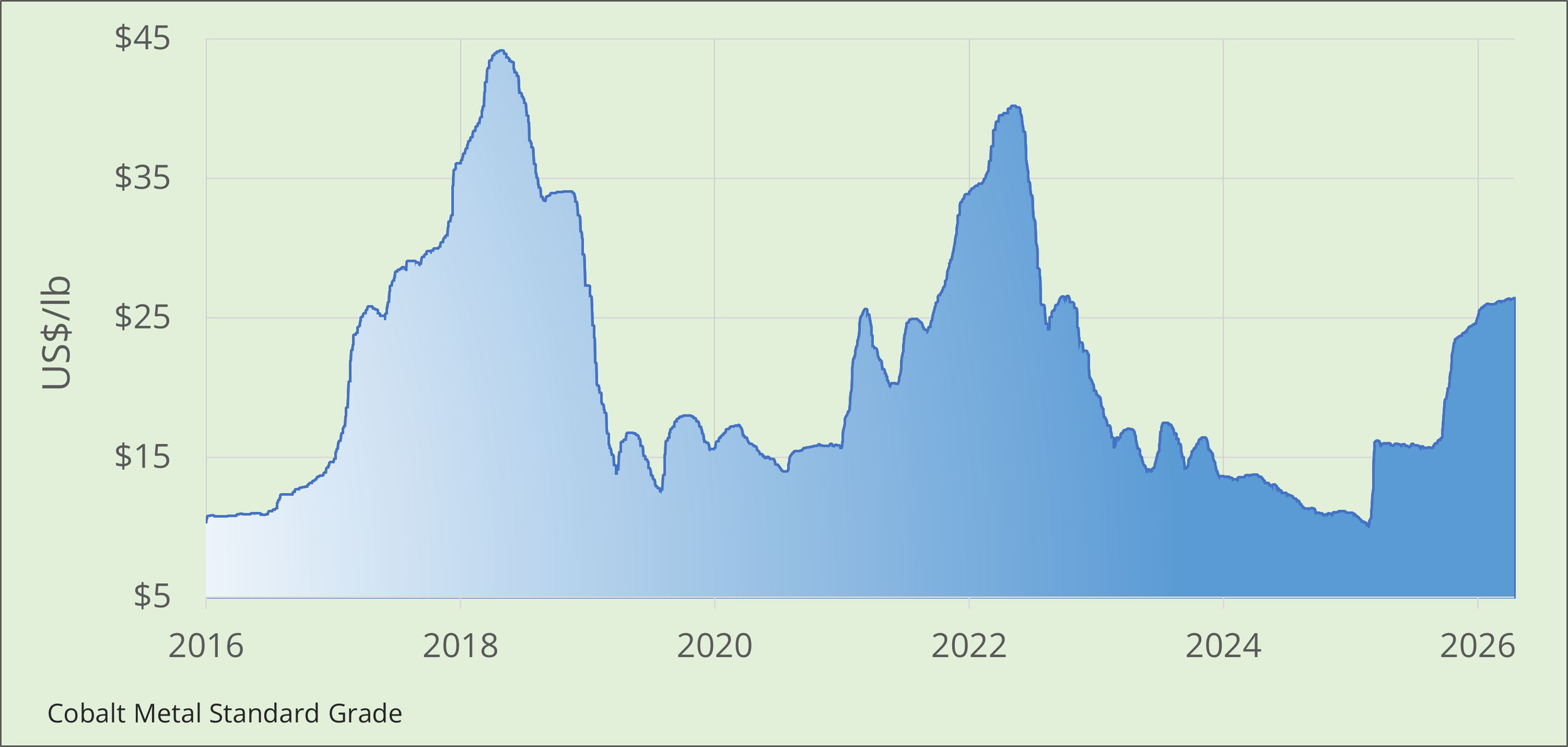

The DRC supply shock: an extraordinary disruption

Even as demand signals were improving, the cobalt market was hit by a supply disruption of historic proportions. The sequence of events unfolded rapidly:

Feb 2025

Following record low prices and significant oversupply, the DRC, which supplies approximately 70% of the world's cobalt, imposed a temporary ban on all cobalt exports.

Mid–Late 2025

The export ban remained effectively in place for the remainder of the year, removing a vast share of global supply from the market.

Late 2025 – Ongoing

The ban was replaced by a quota system that will remain in place until at least 2027. Approved export volumes amount to less than half of the DRC's 2024 production — signalling a multi-year structural tightening of supply.

Early 2026

Intense competition for Congolese cobalt has characterised the early months of the year. While shipments resumed, operational and logistical constraints under the new quota regime slowed execution of allocated volumes.

Source: Fastmarkets

Control is the new battleground

The DRC's dominance of global cobalt supply has made control of mining and refining assets a matter of strategic urgency — not just for commodity traders, but for governments.

Chinese interests currently control approximately 55% of DRC cobalt output and will, naturally, prioritise supply to domestic industries. Recognising the risk this poses to Western defence and energy sectors, the US International Development Finance Corporation has announced joint venture plans with Orion Resources to take a 40% stake in Glencore's two large-scale copper-cobalt operations in the DRC.

But mining control is only part of the equation. Refining capacity, the ability to convert cobalt ore into battery-grade sulphate and industrial-grade metal, matters equally. Western supply chains remain heavily dependent on Chinese refining infrastructure, a vulnerability that policymakers are only beginning to address in earnest.

This dynamic is likely to intensify as governments increase defence and energy independence spending. Cobalt occupies a rare position: it is simultaneously critical to the green transition and to the defence industry.

The world will become increasingly short cobalt

For the first time in years, the cobalt market is not oversupplied. The world is actually short, today.

For much of the past decade, the prevailing narrative on cobalt was one of surplus and falling prices. That narrative has inverted. The combination of export restrictions in the DRC, rising battery demand, and limited near-term development of alternative sources means the market is experiencing genuine tightness, and the structural outlook, stretching to at least 2027, points to sustained constraint.

What happens next

→ EV analysts are beginning to revise demand forecasts upward as oil prices make the economics of electric mobility more compelling

→ The DRC quota system will constrain supply for at least two more years, regardless of demand trends

→ Geopolitical competition for cobalt assets will intensify, with the US, EU, and China each seeking to secure long-term supply

→ Building out downstream processing and refining capacity outside China offers the most rapid path to mobilising new, reliable cobalt supply chains

→ Investors who overlooked cobalt during the oversupply era may find the reset presents a materially different risk-return profile

Cobalt Blue is positioned to be part of the solution

Cobalt Blue’ strategy is to develop the refining and processing infrastructure the Western world urgently needs. With market-leading patented technology, a domestic development pipeline, and a growth strategy extending into the United States, Cobalt Blue is directly addressing the supply chain vulnerabilities the cobalt market now faces.

Strategic Goals

Competitive Strengths

Market-leading, patented minerals processing technology

Cobalt Blue's proprietary processing technology is protected by patents and represents a genuine competitive moat — delivering higher recoveries and lower costs than conventional approaches to cobalt refining. In a market where refining capacity is the critical bottleneck, this is a decisive advantage.

Broken Hill Technology Centre

The company's Broken Hill Technology Centre provides a purpose-built facility to accelerate engineering development and systematically de-risk projects at the technical level — before capital is committed at scale. For investors and project financiers, this translates directly into improved confidence and a stronger basis for funding decisions.