Powering the Green Economy

Cobalt is used in almost every lithium-ion rechargeable device on the planet – from smartphones to smartwatches, tablets to laptops, electric vehicles to solar and battery systems in homes.

You need cobalt if you are sending an email, browsing the internet, checking social media, travelling by car, aircraft, or spaceship.

The metal is also extensively used in superalloys, vital for almost all high-temperature and extreme pressure applications, particularly wind power generation, aviation, and travel industries.

The Cobalt Market

Learn more about Cobalt demand through our extensive report on the global market.

The Cobalt Institute's

Cobalt Factsheet

Cobalt Demand

The new economy has arrived. More people than ever are using technology in their daily lives and this will continue to dominate cobalt demand for the foreseeable future.

Back in the mid-1990s, batteries represented only 1% of cobalt demand (~1,000 tpa). The introduction of lithium-ion technology has changed everything. Now, cobalt demand is around 70,000tpa and as the new economy grows, so will the demand for cobalt.

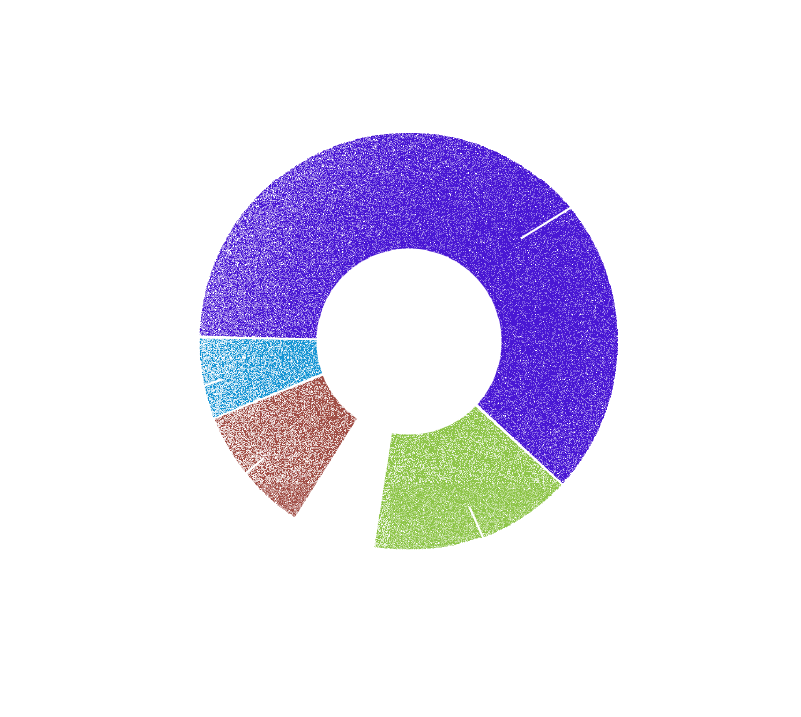

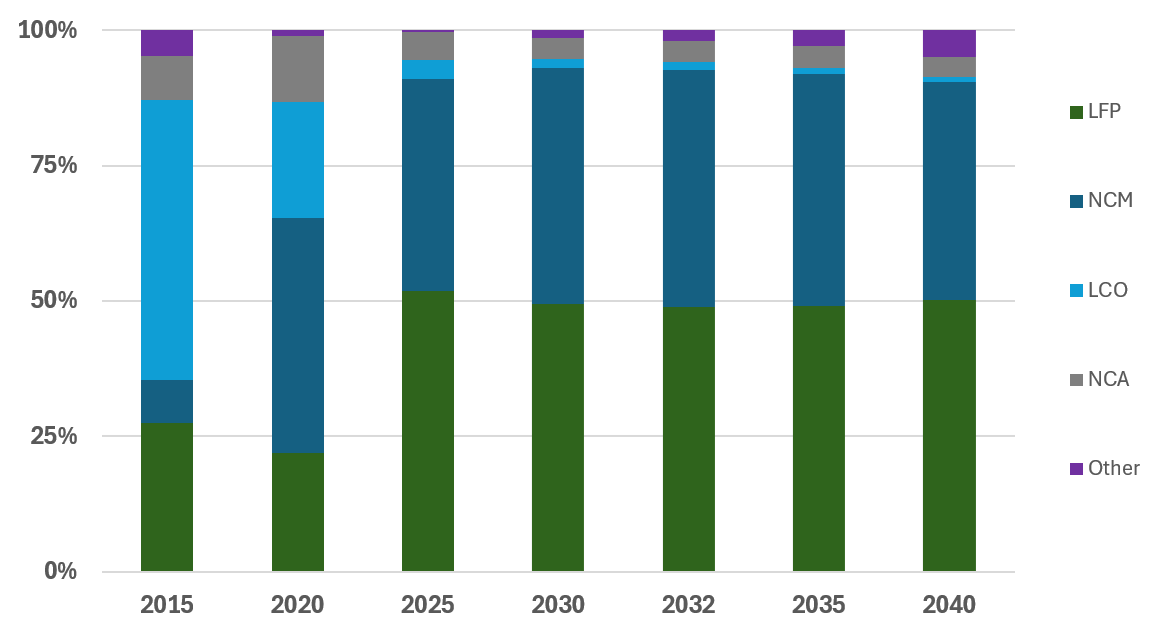

Cobalt demand breakdown

(% end use by industry)

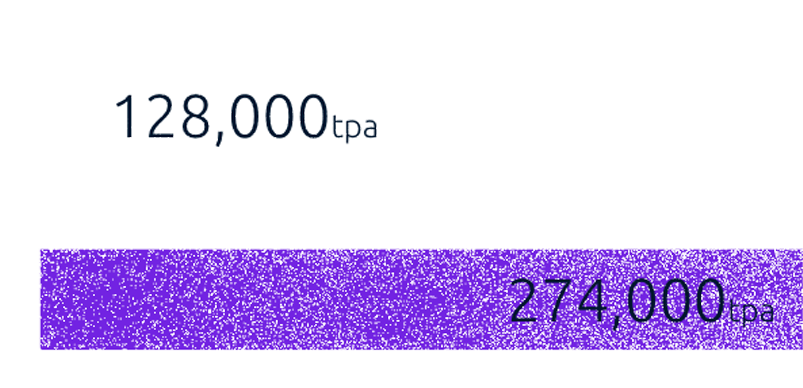

Cobalt demand forecast

(total market size)

Powering the future

Today, most portable applications are powered by cobalt-based lithium-ion batteries. As a result, cobalt demand is now split into ‘new’ and ‘old’ economy drivers.

In the new economy, it’s batteries that require cobalt. Batteries store energy in an era of high energy prices. They play an essential role in the decarbonisation of power grids. They are powering the massive growth of Electric Vehicles (EVs) worldwide.

While still current today, the old economy is more industrial and metallurgical, where cobalt is used in Superalloys, Magnetic Materials, and Catalysts.

Industries

Cobalt batteries

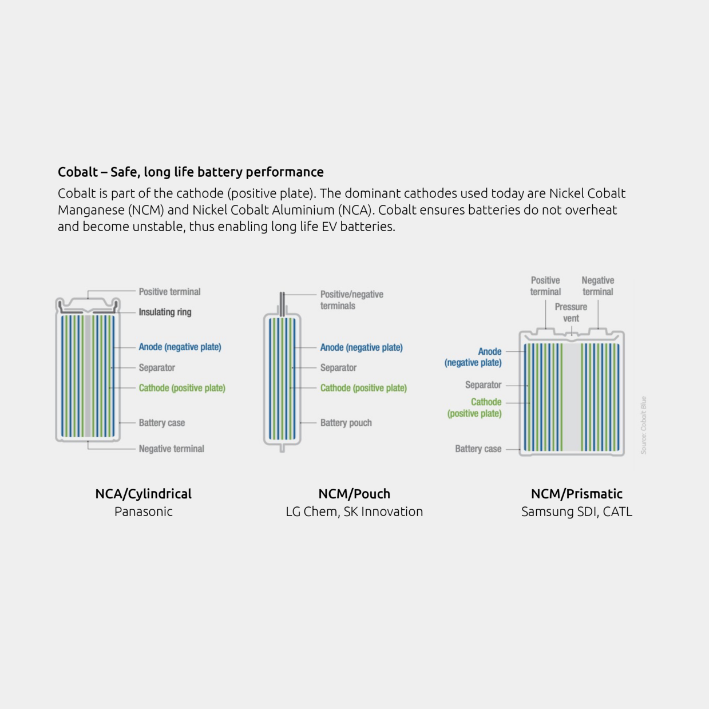

The Sony Corporation first commercialised cobalt-based lithium-ion batteries over 30 years ago. Cobalt-based batteries are an improvement because they have high specific energy vs. weight, they can hold charge and power over time, and are generally maintenance-free.

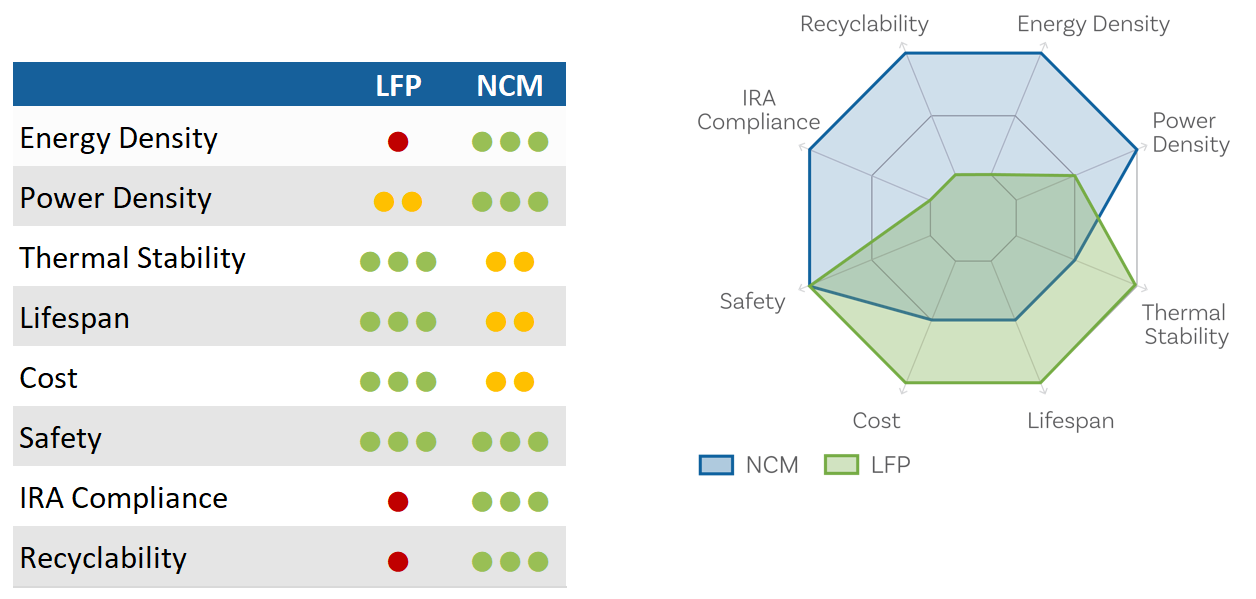

When comparing the different properties of various cathodes: Nickel Manganese Cobalt (NMC) and Nickel Cobalt Aluminium Oxide (NCA) chemistries exhibit superior characteristics over Lithium Cobalt Oxide (LOC) batteries and non-cobalt-based Lithium Iron Phosphate (LFP).

It’s this combination of energy density and stability that makes NMC cathodes the EV batteries of choice. NMC cathodes will supply 85% of the total EV battery market by 2030. While cathodes will undoubtedly contain less cobalt in the future, the sheer growth in EVs will drive strong cobalt demand.

Electric Vehicles (EVs)

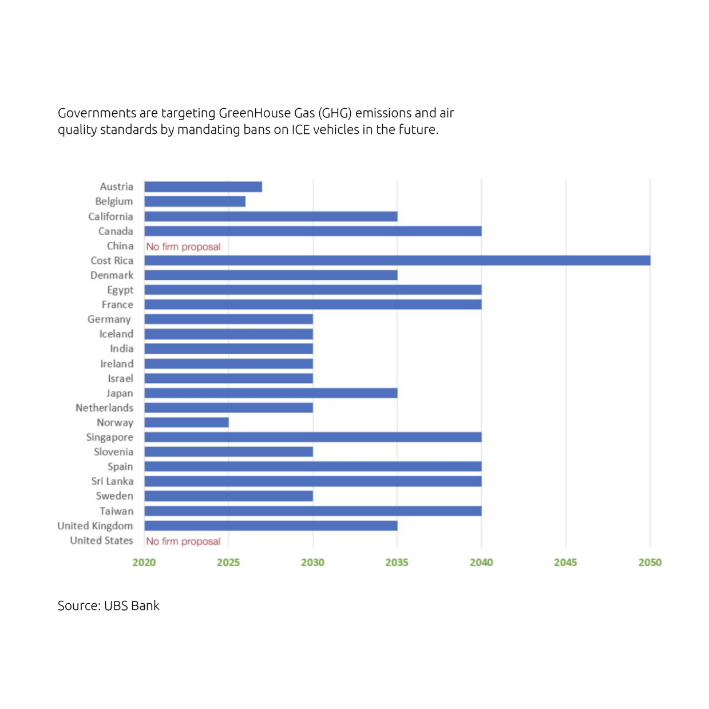

Compared to Internal Combustion Engine (ICE) vehicles, EVs offer cost savings and environmental advantages. Many governments around the world are targeting GreenHouse Gas (GHG) emissions and air quality standards by mandating bans on ICE vehicles in the future.

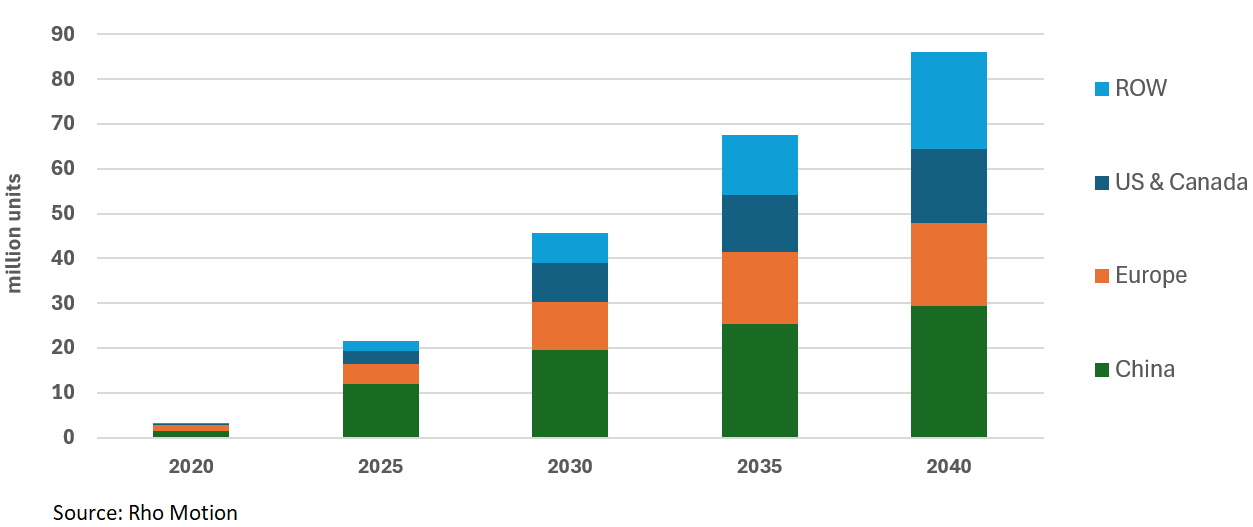

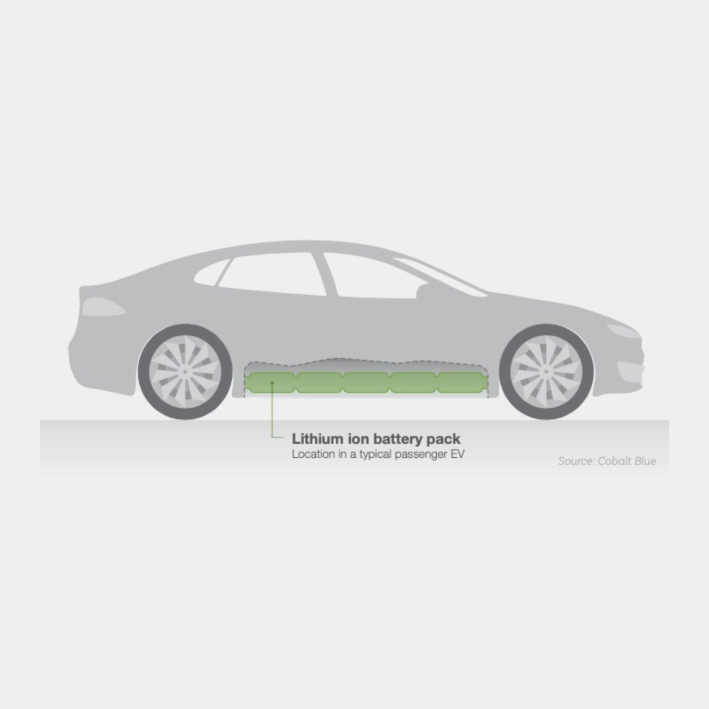

With changing consumer preferences and government incentives, EVs are set to make up more than half the number of global passenger car sales by 2040. They will ultimately dominate the market. In doing so, they will increase the demand for cobalt, which is integral to the lithium-ion battery pack used in hybrid electric vehicles (HEVs), plug-in hybrid electric vehicles (PHEVs), and all-electric vehicles (EVs), including commercial trucks, buses, and electric bikes.